First in a series. A couple of years ago, in an obvious moment of poor judgement, the Kauffman Foundation placed my personal rag on its list of the top 50 economics blogs in America. So from time to time I feel compelled to write about economic issues and the US Labor Day holiday provides a good excuse for doing so now. In a sense you could say I inherited this gig because my parents began their careers in the 1940s working for the US Bureau of Labor Statistics. This first of two columns looks at employment numbers in the current recovery while the second will try to explain why the economy has been so resistant to recovery and what can be done about it.

You’ll see many news stories in the next few days based on a study from the National Employment Law Project detailing how many and what kinds of jobs were lost in the Great Recession and what kinds have come back in the current recovery. Cutting to the chase we lost eight million jobs, have recovered four million of those, but, here’s the problem, the recovered jobs on average pay a lot less than did the jobs that were lost, which is why the US middle class is still hurting.

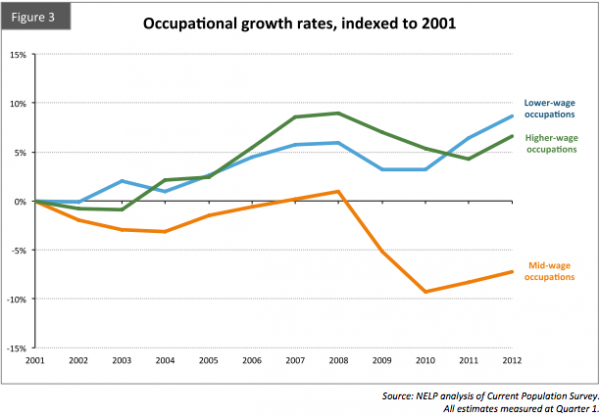

Jobs Lost Not Regained

According to the study, mid-wage jobs such as construction trades, manufacturing and office employees accounted for 60 percent of the employment drop during the recession but made up just 22 percent of the recovery through March 2012. So-called low-wage jobs like retail and food service workers made up 21 percent of the losses but 58 percent of the subsequent growth.

So while we may have regained 50 percent of the lost positions, we’ve regained significantly less than 50 percent of the lost personal income. With less income we have less to spend and spending is what expands economies.

Even more damning, if you look at the chart below that I’ve reproduced is that absolute numbers of both high-wage and low-wage job holders continued to grow through the decade following 9/11 that included two recessions, while numbers of mid-income earners dropped throughout with the exception of one positive blip in 2007.

No wonder the middle class has been decimated.

Previous recessions, we’re told, had more symmetric recoveries. Most of the jobs that were lost were eventually recovered and then some. So what makes this recession different from all the previous ones?

One solid argument might be that in practical terms the Great Recession isn’t really over, so the recovery isn’t either. If we just wait awhile things might get better.

In the current political debate over jobs, for example, there are those who argue staying the course (the Obama campaign) and those who argue for significant, if undefined, changes of course (the Romney campaign). Interestingly both campaigns feel a sense of efficacy -- that full recovery can come.

Of course it can, but will it?

Look at Japan

Our poster child for the current US economy is Japan, which has managed not to fully recover from the recession following its bubble economy of the late 1980s -- 25 years of economic stagnation made tolerable through deficit spending by the state. So it is very possible for the United States to not emerge from the current muck for decades, which is one of the reasons why so much capital sits uninvested on the sidelines earning one percent or less.

Why invest if growth is unlikely?

The jobs added in the current recovery are those that require very little capital. Expanding the third shift at McDonald’s costs a lot less than building a new semiconductor fab.

There are those who argue that many of the higher paying jobs that have not been regained are gone forever for structural reasons -- technology improvements or changes in business culture or the global economy having made them no longer useful. That’s where all the secretaries have gone, we’re told: they were extravagant relics during the Clinton era only to be killed by the Bush economy and unnecessary in the Obama era. That’s how American manufacturing went to China, we’re told.

The unprecedented housing crash and excruciatingly slow recovery of the construction industry explains why there are only half as many construction jobs as there used to be, we’re told, but this too shall pass.

Or will it?

No Entrepreneurial Zeal

I’d argue that what we’ve mainly lost is some aspect of the entrepreneurial zeal of the 1990s. There’s something different about starting a business now compared to then. It’s still exciting, technological and market changes have in many ways made it even cheaper and easier to start new companies and bring innovative products to market, but we just aren’t getting as much wealth-building for our bucks.

Am I alone in feeling this way?

How could a time with higher tax rates be what we hearken back to as a golden age of entrepreneurism? Some might argue it wasn’t that at all: what Cringely longs for is just another bubble, in this case the dot-com bubble.

Yes, the dot-com bubble was fun, just as the Japanese enjoyed buying-up half of the world’s golf courses in the 1980s, but that’s not what I am talking about here.

I have a fear that true recovery has been so resistant because we’ve somehow wounded our economy making it resistant to recovery. And if we don’t find a way to heal those wounds true recovery will never happen.

What I believe to be the surprising sources of this national pain and possible ways to heal it are the topics of my next column.

Reprinted with permission

Photo Credit: ARENA Creative/Shutterstock